How to Start Investing in Europe with €10

Beginner’s Guide

This post may contain affiliate links. We may earn a commission at no extra cost to you.

The Night I Decided to Stop Letting My Money Do Nothing

Dublin, 2017. End of a long shift cleaning hotel rooms. Feet hurting. Phone in hand. Scrolling through nothing in particular.

Then a short video of someone talking about money. He said something simple that was hard to forget:

“You don’t need to be rich to invest. You just need to start.”

The first reaction was to laugh. Invest? Coming from Mangueira, Rio de Janeiro — a neighbourhood where investing was something people in suits did, people with fancy degrees, people who understood complicated words — it felt like something for other people. Not for someone like me, working shifts and learning a new language.

But then a different thought: I was in Europe. I had a bank account. I had a phone. And I had €20 I could spare without too much stress.

That was the moment everything changed.

This guide is written for anyone who has had that same reaction — who has seen investing as something for other people, something complicated, something that requires money you do not have. It is written to show that none of that is true, and to explain exactly how to start from where you are right now.

What Is Investing and Why Does It Matter?

Investing means putting your money into something — shares in companies, funds, property — with the expectation that it will grow in value over time. Instead of sitting in a bank account earning almost nothing, your money is working.

The most important reason to care about this is something most people learn too late: inflation.

If you leave €100 in a bank account for a year, those €100 will buy slightly less at the end of the year than they did at the beginning. Prices go up. Your money stays the same number. In real terms — in what that money can actually buy — you have less.

Over five years, this effect compounds. Over twenty years, it is significant.

Investing is the response to that problem. When your money is invested in assets that grow, it keeps pace with inflation or outpaces it. Your purchasing power is protected and, over time, increased.

This is not about becoming wealthy overnight. It is about making sure the money you work hard for does not quietly lose value while sitting still.

The Investor’s Best Friend: What Is an ETF?

Most beginner investing guides jump straight into complicated terminology. This one will not. There is one concept worth understanding before anything else, and it makes everything simpler.

ETF stands for Exchange Traded Fund. Ignore the name. Here is what it actually means.

Imagine you want to invest in companies but you are not sure which ones will do well. If you put all your money into one company and that company struggles, you lose a lot. But if you spread your money across many companies, one company struggling does not hurt you nearly as much.

An ETF is a ready-made spread. When you buy one ETF, you are automatically buying a tiny piece of dozens or hundreds of companies at once. You do not choose which companies — the ETF already contains them, following a set list called an index.

A simple analogy: instead of buying one piece of fruit and hoping it is the best one, you buy a basket with many different fruits. If one goes bad, the others are still fine.

Common ETFs Available in Europe

Clean infographic showing best ETFs for beginners in Europe, including iShares MSCI Europe, Vanguard S&P 500, and Amundi Euro Stoxx 50, with simple explanations.

The word “UCITS” appears on most ETFs sold in Europe — it just means the fund follows European regulations and is legally available to investors here.

Why ETFs Are the Right Starting Point for Beginners

- Built-in diversification. One purchase spreads across many companies automatically.

- Low fees. ETFs typically charge between 0.07% and 0.25% per year — a tiny fraction of what traditional investment funds charge.

- Simple to buy. Through a modern broker app, buying an ETF takes the same steps as any other purchase.

- Start with very little. Some platforms let you buy fractional ETF shares from €1.

If you take one thing from this guide, take this: ETFs are where most beginners should start. Not individual stocks. Not complex products. A simple, diversified ETF bought regularly over time.

How Does Investing Actually Work?

The mechanics are simpler than most people expect. Here is the process from beginning to end.

You open an account with a broker. A broker is an app or website that gives you access to investment markets. You do not go to a physical building — everything happens on your phone or computer.

You deposit money. You transfer money from your regular bank account into your broker account. This can be as little as €1 on some platforms.

You choose what to buy. You search for the ETF or stock you want, enter how much you want to spend, and confirm the purchase. The shares appear in your account.

Your investment changes in value over time. The price of your shares goes up and down based on how the underlying companies are performing. Over the long term, well-diversified investments have historically gone up.

You decide when to sell. You can sell your shares at any time and receive the current value. The profit (or loss) from the difference between what you paid and what you received is what you actually earn.

The key insight most beginners miss: the majority of the work happens at the beginning, when you set things up. After that, the main job is to keep adding money regularly and not panic when prices move.

Why It Is Worth Starting Now, Even With Little Money

There are several reasons why starting small and starting now is better than waiting.

Time is the most valuable factor. A concept called compound growth means that the earlier you invest, the more time your money has to grow — and growth builds on previous growth. €100 invested today at 6% annual growth becomes €101 more than €100 invested one year from now. Over twenty years, the gap between starting today and starting in five years is significant.

The habit matters more than the amount. Investing €20 per month consistently teaches you more than investing €2,000 once. You learn how the market moves. You develop a calm relationship with price fluctuations. You build the discipline of setting money aside before spending it.

Europe makes it genuinely accessible. Modern broker apps in Europe have removed nearly every practical barrier. No minimum deposits on most platforms. No complicated paperwork. Fractional shares mean you can invest in expensive company stocks with just a few euros.

Immigrants and new residents can participate. If you have a European bank account and proof of residence, you can open an investment account through the major platforms. You do not need to be a citizen. Many people in this community assume investing is not available to them — it is.

The alternative is inflation. Leaving money in a low-interest bank account is not a neutral choice. It is a slow loss of value. Doing nothing has a real cost.

Step-by-Step: How to Start Investing in Europe

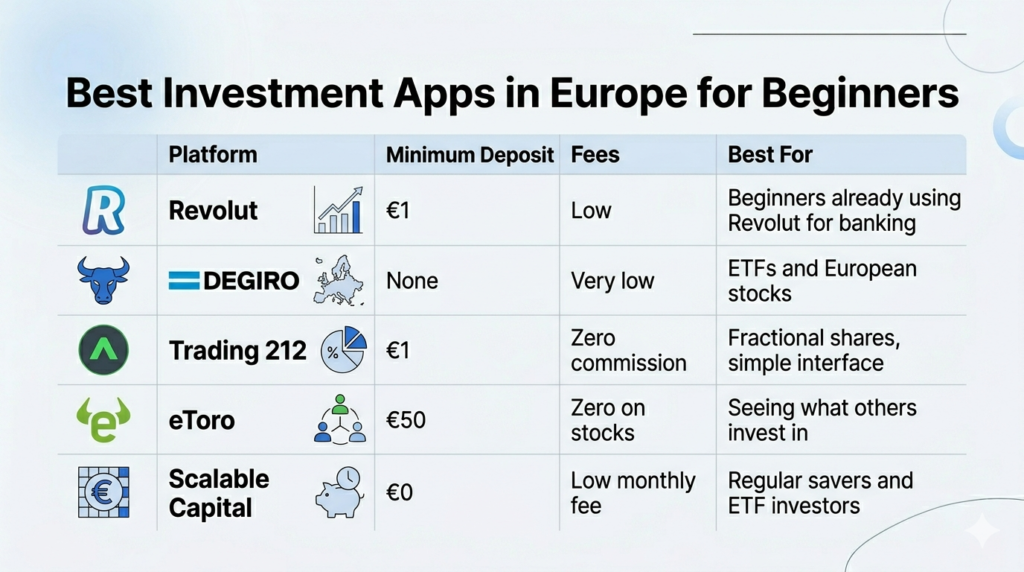

Step 1 — Choose a Broker Platform

A broker is the platform where you buy and sell investments. There are several good options in Europe, each with slightly different features:

Clean infographic showing best investment apps in Europe for beginners, including Revolut, DEGIRO, Trading 212, eToro, and Scalable Capital, with fees and features.

For most beginners, starting with the simplest option makes sense. If you already use a digital banking app with an investing feature built in, starting there removes the need to learn an entirely new platform. Once you have invested for a few months and feel comfortable, you can always open a second account with a specialist broker for lower fees on larger amounts.

Step 2 — Open and Verify Your Account

The process is similar across all platforms:

- Download the app or visit the website

- Enter your personal details

- Verify your identity — you will need to take a photo of your ID (passport or national ID card) and a quick selfie

- Submit and wait for approval — this typically takes between a few hours and two days

Once approved, your account is ready to receive funds and make purchases.

Step 3 — Deposit Your Starting Amount

Transfer money from your regular bank account into your broker account. The amount matters less than the habit of doing it.

A practical starting point is whatever you can genuinely spare without creating financial stress. For some people, that is €10. For others, €50. The number is less important than the fact that you do it.

Set up a regular transfer if your platform allows it — same amount, same day each month. Automating this one step removes the decision from the equation and makes investing a background habit rather than a monthly task to think about.

Step 4 — Choose Your First Investment

For a complete beginner, the simplest and lowest-risk approach is one broad ETF. Search for any of the following on your chosen platform:

- iShares Core MSCI Europe UCITS ETF — exposure to a wide range of European companies

- Vanguard S&P 500 UCITS ETF — exposure to the 500 largest US companies

- iShares Core MSCI World UCITS ETF — a global spread covering companies from many countries at once

Any of these gives you immediate diversification. You are not betting on one company or one country. You are buying a slice of many economies at once.

If you want to split your investment between two of these, that is fine too. But starting with one is simpler, and simple is better when you are learning.

Step 5 — Buy and Then Leave It Alone

Complete your first purchase. Watch the shares appear in your account.

Then close the app.

This is the step most beginners struggle with. The temptation to check daily — to watch the number go up and then down and then slightly up again — is strong. But daily price movements are noise. They are not information about whether your long-term investment is doing well or badly.

Check your portfolio once a month at most. Add money once a month. Do not sell when the price drops. These three behaviours are what separate investors who succeed over the long term from those who panic and lose money.

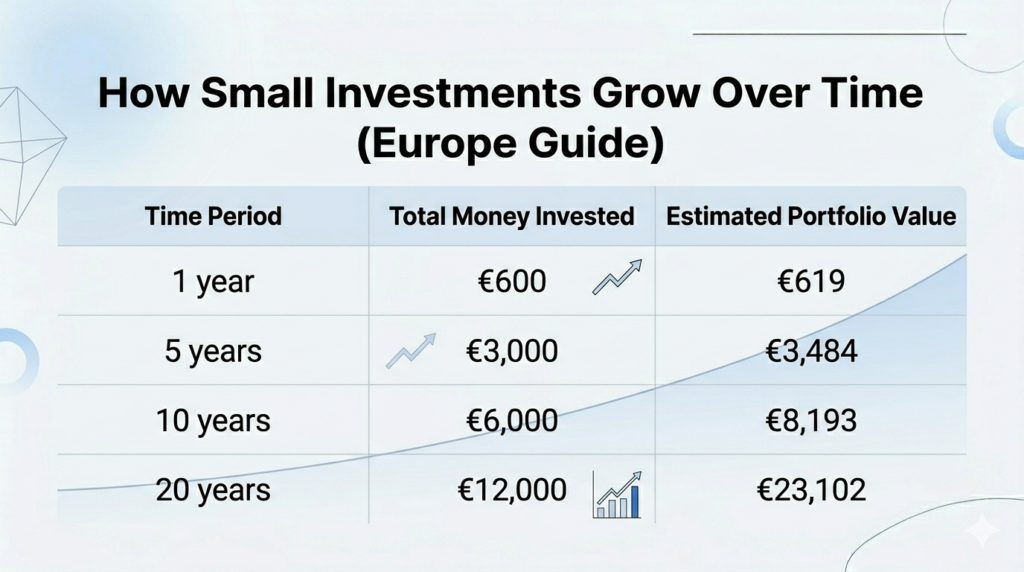

What Happens to Your Money Over Time: Real Numbers

Numbers make this concrete. Here is what a consistent €50 per month investment looks like over time, assuming an average annual return of 6% — a conservative figure based on historical stock market performance.

Infographic showing how small investments grow over time in Europe, comparing money invested versus portfolio value over 1, 5, 10, and 20 years.

At the 20-year mark, you have invested €12,000 of your own money. The portfolio is worth €23,102. The difference — €11,102 — came from growth, not from you working more hours.

This is what compound growth does over time. The longer it runs, the larger the gap between what you put in and what you have.

These are not guarantees. Markets fluctuate, and past performance does not guarantee future results. But this is what consistent, diversified investing has historically produced for patient investors.

What About Buying Individual Company Shares?

ETFs are the starting point, but once you are comfortable, individual company shares are worth understanding.

The traditional barrier was price. A single share in a large European company could cost hundreds or even thousands of euros — far out of reach for most beginners.

Fractional shares changed this. Most modern broker platforms now allow you to buy a fraction of a share. You invest a fixed amount — say, €15 — and you receive the equivalent fraction of one share. You own a tiny piece of the company, earn a proportional dividend if the company pays one, and benefit from the same price growth as any other shareholder.

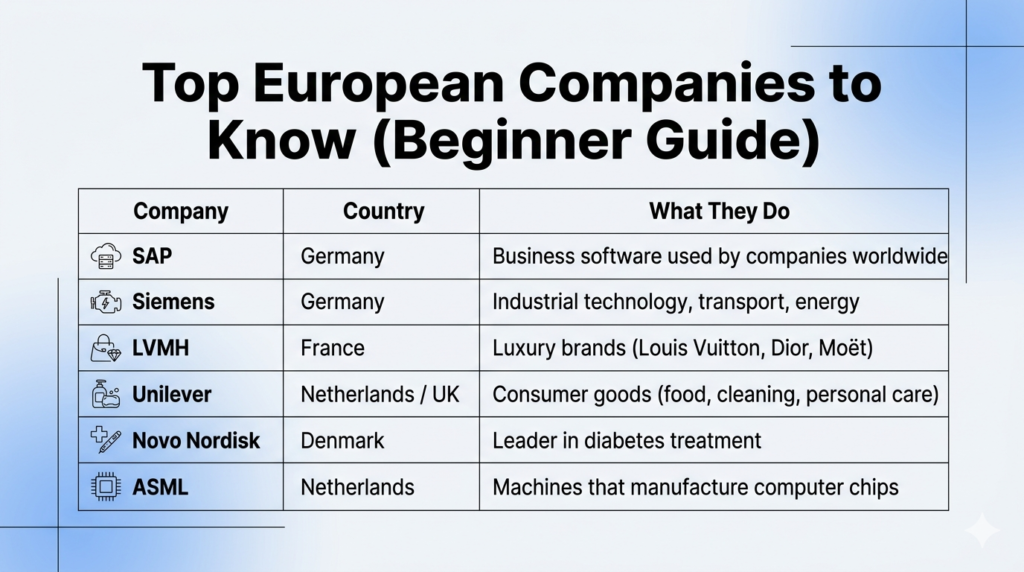

Major European Companies Worth Knowing

Infographic showing top European companies including SAP, Siemens, LVMH, Unilever, Novo Nordisk, and ASML, with their country and business focus.

These are some of Europe’s most established companies, with long track records. Investing in individual companies carries more risk than a diversified ETF — if one company underperforms, your investment suffers more than it would in a broad fund. But fractional shares make them accessible as a small portion of a diversified portfolio once you have learned the basics.

Common Questions, Answered Honestly

“I only have €10. Is it worth it?”

Yes. Ten euros today teaches you something that cannot be taught any other way — you experience how markets move, how investing feels, and what your emotional reactions are to price changes. The habit and knowledge you build are worth more than the amount. Next month, another €10. In a year, €120 plus whatever growth has occurred — and a year of investing experience.

“What if I lose everything?”

If you invest in a broadly diversified ETF tracking a major index, history strongly suggests you will not lose everything. Individual companies can fail. Entire diversified indexes tracking hundreds of companies have never gone to zero. They have had severe drops — the 2008 financial crisis, the 2020 pandemic — but they have always recovered and continued growing. The risk of a total loss from a diversified ETF is very low. The risk of a temporary loss in value is normal and expected.

“Can immigrants invest in Europe?”

Yes. You need a European bank account and proof of residence. Most major broker platforms accept non-citizens who are legally resident in a European country. If you have a bank account and an address, you can invest.

“Do I have to pay tax on investment profits?”

In most European countries, yes. The rules vary significantly between countries — some tax dividends and capital gains differently; some have allowances below which gains are not taxed; some tax ETFs differently from individual stocks. Keep records of everything you buy and sell from the start. When you sell investments at a profit, research your country’s specific rules, or ask in a local expat or finance group where others have navigated the same system.

“How long should I leave money invested?”

Think in years, not months. A minimum of five years is the standard guidance for money in stocks or ETFs — this gives enough time for temporary drops to recover. The longer you can leave money invested, the better the expected outcome. Money you might need within two or three years should not be in the stock market.

Tips to Do Better and Mistakes to Avoid

Mistakes That Cost Beginners Money

Waiting for the perfect moment to start. There is no perfect moment. Markets are always either rising, which feels expensive to enter, or falling, which feels scary to enter. The research is clear: time in the market — consistently investing over years — produces better outcomes than trying to time the market perfectly. Start now with whatever you have.

Checking your portfolio every day. Daily price movements are meaningless for a long-term investor. They create anxiety, tempt you to make emotional decisions, and teach you nothing useful. Set a monthly check-in and stick to it.

Selling when the market drops. The moment when prices fall is the moment when inexperienced investors sell and experienced investors buy more. Selling during a drop locks in your loss. Staying invested — and ideally buying more — is how patient investors benefit when the market recovers.

Choosing platforms with high fees on small amounts. Some platforms charge fees that represent a large percentage of a small investment. Always check the fee structure before depositing money. The established platforms listed in this article have competitive, transparent fee structures.

Trying to pick hot stocks or following tips. Individual stock picking is difficult even for professional fund managers. Following social media tips or “hot stock” recommendations is how beginners lose money. ETFs first. Individual stocks only after you understand the basics and with a small portion of your total investment.

Habits That Make a Real Difference

Invest the same amount on the same date every month. This is called “dollar-cost averaging” in investment terminology, but the practical effect is simple: you stop thinking about whether now is a good time to invest. You just do it. Some months you buy at a higher price, some months at a lower price. Over time, it averages out to a reasonable entry point.

Reinvest dividends rather than withdrawing them. Many ETFs and stocks pay dividends — a small share of company profits distributed to investors periodically. If your platform allows automatic dividend reinvestment, enable it. If not, manually use dividend payments to buy more shares. This is how compound growth accelerates over time.

Keep a simple record. A basic spreadsheet with what you bought, when, and at what price is enough. It gives you a clear picture of your portfolio, makes tax season significantly easier, and — perhaps most importantly — shows you the progress you are making, which keeps you motivated during the slow early months.

Increase your contribution as your income grows. Starting with €20 per month is fine. But as your income situation improves, increase the amount. Going from €20 to €50 per month, or from €50 to €100, has a large impact on long-term outcomes.

The Mindset Shift That Matters More Than the Money

The practical side of investing is straightforward. The harder part is mental.

Many people — immigrants especially, people who grew up with financial uncertainty, people who have had to fight for every euro — find it difficult to think long-term when short-term pressures are real. Sending money home. Covering rent. Managing on an uncertain income.

But there is a shift that happens when you start investing, even with small amounts. You begin to see yourself not just as someone surviving in a new country, but as someone building something here. Someone who has a stake in the future. Someone who belongs in the financial system, not outside it.

That feeling — of actively building rather than just getting by — is real. And it compounds, just like the money does.

And Now, What To Do Next?

Investing in Europe is accessible to anyone with a bank account, a phone, and a small amount of money they can spare each month. The platforms are simple. The minimum amounts are low. The concepts, once explained clearly, are not complicated.

The gap between knowing this and actually starting is the only real barrier.

Here is what to do this week:

- Choose one of the platforms mentioned in this guide — Revolut, DEGIRO, Trading 212, or another that suits your situation

- Open and verify your account — it takes less than 20 minutes

- Deposit your starting amount — €10, €20, or €50, whatever feels comfortable

- Search for one of the simple ETFs mentioned in this guide and buy your first shares

- Set a reminder to add the same amount on the same date next month

Then leave it alone.

Check back in a month. Add more money. Repeat.

The person who starts with €20 today, keeps going, and never panics will finish in a much better position than the person who waits until they feel ready — which, without starting, never comes.

Your future self is waiting for a decision you can make today.

What is your biggest question or worry about investing? Drop a comment below — questions that come up here often become future articles, and there are no questions too basic to ask.

EuroSideHustle helps people in Europe — including immigrants and beginners — build real income online. Explore more guides at EuroSideHustle.com.